Refinancing a mortgage can feel overwhelming, but for many homeowners, it’s a smart way to reduce monthly payments, access cash, or shorten the loan term. If you’ve been asking yourself, “when should I refinance my mortgage?”, you’re not alone. Millions of Americans face this decision each year, trying to balance interest rates, personal finances, and long-term goals. In this guide, we’ll walk you through exactly when refinancing might make sense and how to approach it like a savvy homeowner.

Understanding Mortgage Refinancing

Before diving into the signs, it’s important to understand what it means to refinance your mortgage. Refinancing involves replacing your existing mortgage with a new one, often with different terms. The goal could be:

- Lowering your interest rate to reduce monthly payments

- Switching from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage

- Shortening the loan term to pay off your mortgage faster

- Tapping into your home’s equity through a cash-out refinance

By refinancing, you could save thousands of dollars over the life of your loan, improve cash flow, or consolidate high-interest debt.

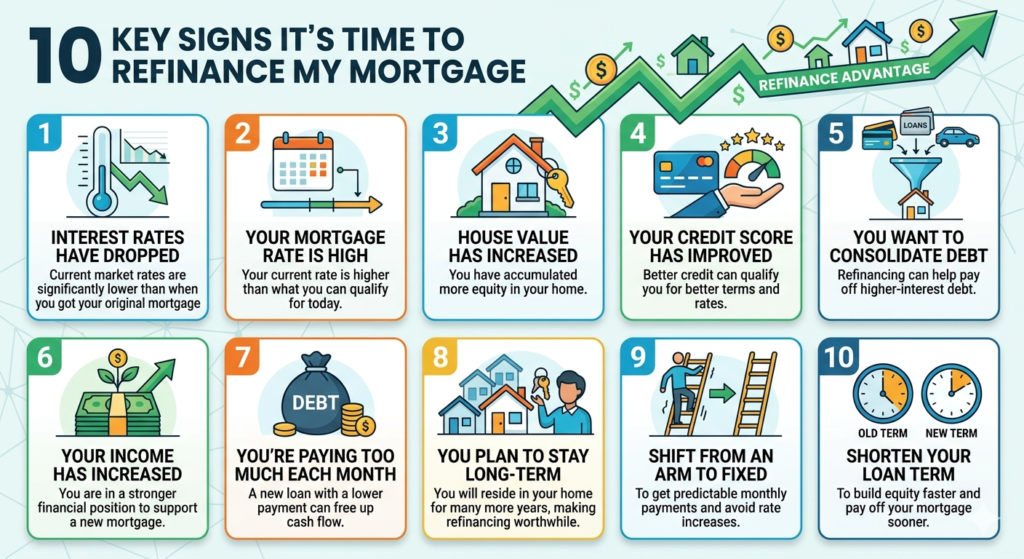

1. Interest Rates Have Dropped Significantly

One of the clearest reasons to refinance my mortgage is when market interest rates fall below your current rate. Even a drop of 0.5% can make a noticeable difference in monthly payments.

Example Table: Potential Savings from Refinancing

| Current Rate | New Rate | Loan Amount | Original Monthly Payment | New Monthly Payment | Monthly Savings | Annual Savings |

|---|---|---|---|---|---|---|

| 5.5% | 4.0% | $300,000 | $1,703 | $1,432 | $271 | $3,252 |

| 6.0% | 4.5% | $400,000 | $2,398 | $2,027 | $371 | $4,452 |

If interest rates drop significantly, refinancing may be worth considering to lock in savings.

2. You Want to Change Loan Terms

Another key reason to refinance my mortgage is adjusting the term of your loan. If you have a 30-year mortgage but want to pay it off in 15 years, refinancing can shorten the term. While your monthly payments may increase, you could save tens of thousands in interest over time.

Conversely, if you’re struggling with high payments, refinancing from a 15-year to a 30-year mortgage could reduce your monthly obligation, freeing up cash for other priorities.

3. Your Credit Score Has Improved

Lenders consider your credit score when determining your interest rate. If your credit score has improved significantly since you first got your mortgage, refinancing my mortgage could qualify you for a better rate, even if market rates haven’t changed drastically.

Tip: Check your credit score before applying. A score increase of 50–100 points can result in meaningful savings.

4. You Want to Switch from ARM to Fixed-Rate

Adjustable-rate mortgages can be appealing initially due to lower rates, but they can become risky if rates rise. Refinancing my mortgage from an ARM to a fixed-rate mortgage provides predictable payments and protects against interest rate volatility.

Example: A homeowner with a 5/1 ARM paying 3.5% could refinance to a 30-year fixed rate at 4.0%. While the rate is slightly higher, stability often outweighs the cost.

5. You’re Planning Major Life Changes

Life events such as getting married, starting a family, or retiring may influence when to refinance my mortgage. Refinancing could free up monthly cash flow, consolidate debt, or allow for a shorter loan term to pay off the house before retirement.

6. You Want to Tap Into Home Equity

If your home has appreciated and you need cash for renovations, education, or debt consolidation, a cash-out refinance can be useful. This option increases your loan balance, so it’s important to consider whether the benefits outweigh the costs.

Cash-Out Refinancing Table

| Home Value | Existing Mortgage | Loan-to-Value | Cash Available |

|---|---|---|---|

| $400,000 | $250,000 | 80% | $70,000 |

| $500,000 | $300,000 | 75% | $75,000 |

Always factor in closing costs and new monthly payments when considering a cash-out refinance.

7. You Want to Eliminate Private Mortgage Insurance (PMI)

If your home value has risen and you now have more than 20% equity, refinancing my mortgage can help remove PMI. Eliminating PMI reduces monthly costs and increases your overall savings.

8. Closing Costs Are Affordable

Refinancing comes with closing costs, usually 2–5% of the loan amount. Even if rates are favorable, refinancing may not make sense if the costs outweigh potential savings. Calculate the break-even point to determine if refinancing is worth it.

Break-Even Example Table

| Loan Amount | Closing Costs | Monthly Savings | Break-Even Point (Months) |

|---|---|---|---|

| $300,000 | $6,000 | $200 | 30 |

| $400,000 | $8,000 | $300 | 27 |

If you plan to stay in your home beyond the break-even point, refinancing may be financially beneficial.

9. You’re Consolidating High-Interest Debt

Some homeowners refinance my mortgage to consolidate credit cards or personal loans with high interest rates. This strategy replaces multiple payments with a single, lower-interest mortgage payment, simplifying finances and potentially saving money.

10. Timing and Market Conditions

Finally, consider broader economic factors. If interest rates are historically low and expected to rise, acting sooner rather than later can secure better rates. Likewise, if the housing market is strong and home values have risen, you may benefit from refinancing my mortgage for both rate reductions and access to equity.

Steps to Refinance My Mortgage

- Evaluate Your Goals: Lower payments, shorten term, cash-out, or eliminate PMI.

- Check Your Credit Score: Higher scores yield better rates.

- Calculate Potential Savings: Use online refinance calculators.

- Compare Lenders: Request multiple quotes and review terms.

- Apply and Lock Rate: Submit documents and lock in the rate.

- Close on New Loan: Sign paperwork, pay closing costs, and start new payments.

Frequently Asked Questions

Q1: How often can I refinance my mortgage?

You can refinance as often as it makes financial sense. However, frequent refinancing may not be cost-effective due to closing costs.

Q2: Will refinancing my mortgage affect my credit score?

Yes, refinancing involves a credit inquiry, which may temporarily lower your score. Over time, timely payments can improve it.

Q3: Is refinancing worth it if I plan to sell soon?

It depends on the break-even point. If you sell before recouping closing costs, refinancing may not save money.

Q4: Can I refinance with bad credit?

Yes, but interest rates will be higher. Some government programs may help borrowers with lower scores.

Q5: What is the typical refinancing process timeline?

It usually takes 30–45 days, depending on lender and document availability.

Conclusion

Knowing when to refinance my mortgage can make a significant difference in your financial well-being. From lower interest rates to accessing home equity, the right timing depends on your goals, current mortgage terms, and market conditions. Always calculate savings versus costs, consider your long-term plans, and work with a trusted lender to ensure the refinance aligns with your financial strategy.

By following these insights, you can make informed decisions and potentially save thousands while gaining peace of mind with a mortgage that better fits your life.